Buying a “starter home” is treated as a rite of passage in our culture. What better way to prove that you’re a responsible, financially stable adult than by buying a house? After all, it’s a solid investment and better than renting, right?

We can all probably list a number of reasons we’ve heard for buying your first starter home - “Why rent when you can own?” “Renting is just paying someone else’s mortgage.” “Renting is wasting money that you could be putting towards equity in your own home.” “It’s a buyer’s market.” “Interest rates have never been lower, you better buy now!” We hear these positive justifications for jumping into homeownership so often that they’ve become conventional wisdom, even cliche.

Ask yourself, though, where do you often hear these types of sales pitches for buying a home? Real estate agent advertisements? Bank and mortgage lender advertisements? Homebuilder and subdivision advertisements?

There are lot of business entities out there, or rather, entire industries, that make big money when homes are purchased, and they rely heavily upon convincing more and more individuals to enter the homebuying market.

Who profits when you choose not to buy? Essentially nobody (except perhaps your local landlord, who would quickly find a new renter if you left). So because there is no money in it, nobody is out there giving you the opposite perspective as to when it would be most prudent to take the step towards homeownership.

Does it now start to make sense why the urge to buy a home as soon as possible seems so pervasive in our culture? Multi-billion-dollar industries are depending on you to take on a mortgage and will market aggressively towards you until you’re convinced to do so. Put simply, follow the money.

Putting that aside, let’s look at the dollars and cents. How do the costs and benefits of buying and selling starter homes break down?

What is a “Starter Home”?

To begin, think about the connotations of the loaded term “starter home.” Being a “starter” means that you know going into purchasing it that you won’t be there forever, probably just a few years, until you can parley its sale into the purchase of a bigger, better home. You take for granted that you’ll be able to easily sell the property whenever you are ready to move on. And it also means that it’s affordable and within your present modest means, usually because it’s small or in need of repairs. You take for granted that you will be able to sell it for at least a small profit, to cover your expenses, when you want to move on. But is it ever that easy?

Costs vs. Appreciation

The myth of buying a home versus renting is that renting is flushing money down the drain, whereas owning a home means you pay into the equity of your home and then make all your money back and more when you sell it. There are a number of reasons why that actually doesn’t happen.

First, very little of your monthly mortgage payment actually goes against your principal.

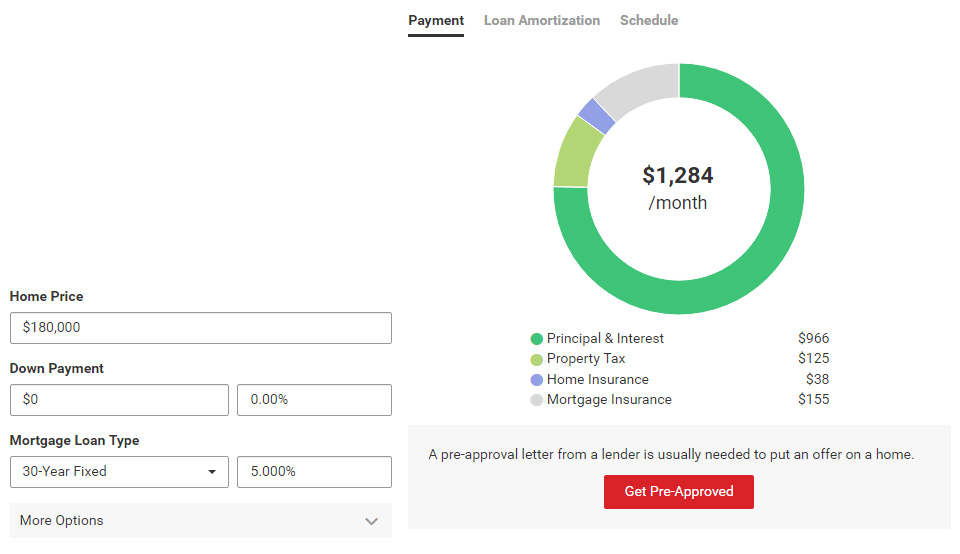

Let’s say you purchased a modest $180,000 home with a 30-year fixed mortgage at a 5% market interest rate. Using the mortgage calculator on Realtor.com, your monthly mortgage payment will come to around $1,284 per month, depending on your area. Sounds cheaper than renting, right? And you’re paying your monthly $1,284 towards your $180,000 home price, right?

Not really. If you look at the breakdown in the pie chart, you will see that your calculated mortgage payment will be comprised of either 4 or 5 parts - principal, interest, home insurance, property taxes, and sometimes mortgage insurance if that was a condition of your mortgage. Insurance and taxes will vary based on your area, and could be higher if you’re in a high-tax area or in an area at risk for natural disasters. But no matter what, those hundreds of dollars are mandatory fees and will not be recouped.

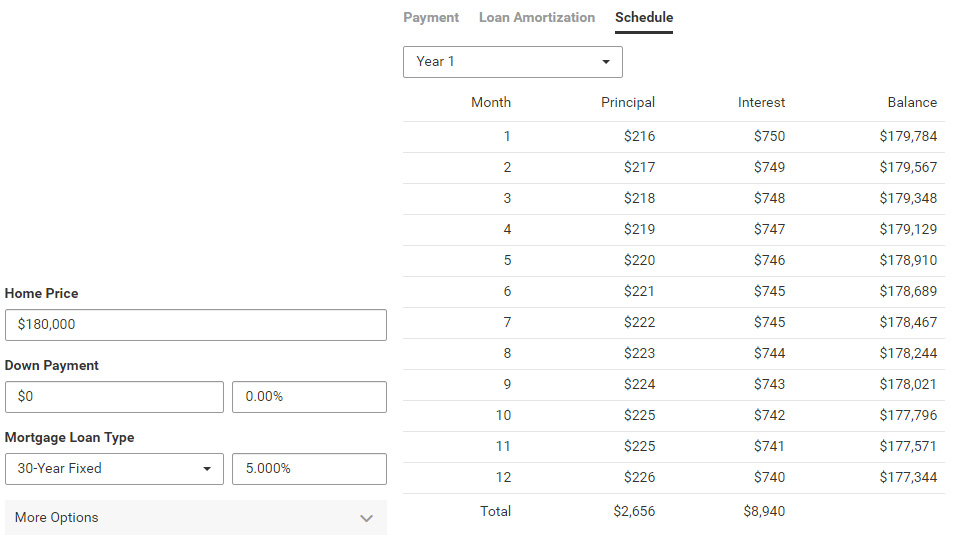

Okay, but that $966 out of the $1,284 goes towards the purchase price, right? That’s still a lot into the house’s equity, right? Well, Realtor.com is in the business of making mortgages look really appealing, so they lump “Principal & Interest” into one measurement of the pie chart. But if you click on the “Schedule” tab, you can see how that “Principal & Interest” lump amount actually breaks down. In actuality, the bulk of that “Principal & Interest” payment is interest on the loan, which, in other words, is pure profit for the bank. In this example, during your first month’s payment, $750 will go directly into the bank’s coffers, and just $216 will go towards paying down the principal amount of your loan. After a year, you will only have put $2,656 worth of equity into your home, with the other $12,752 going to taxes, insurance, and bank profits.

Of course, homeownership comes with its financial responsibilities too. Should you need to pay for inevitable repairs, those expenses will effectively negate some of the saved equity.

But let’s say you had some good luck and by some miracle, you didn’t need to pay for any major repairs during your time in your starter home. Then, say, after 3 years, your life changed - either you needed more space for a growing family or needed to relocate for a better job - so it’s time to sell your starter home.

Easy to Get In, But Hard to Get Out

After 3 years, you will have put roughly $9,000 worth of equity towards the principal of your loan (unless you voluntarily paid extra towards your principal above your minimum payment, which seems unlikely since many starter home-buyers max out their budgets). That $9,000 equity comes to about 5% of your original purchase price.

You will likely need the help of a real estate agent to list and sell your home. The going rate for realtor commission is 6%, which is 3% for the selling agent and 3% for the agent that found the buyer. So if you just sold your home for the purchase price you originally paid for it, you would lose $1,800 on the sale. Ouch.

But let’s assume that you bought and sold during a period of economic growth and improving housing market (which was very much not the case 10 years ago, but things are better, for now). How much does your home have to have appreciated just to break even on the sale?

Above and beyond realtor commission fees, there are a number of fees associated with selling a home. Oftentimes when you buy a home, a motivated seller will pay for these closing costs himself/herself to sweeten the deal for the potential buyer, which means you don’t really have a grasp when buying a home just how much the transaction can cost. But now, as the seller, it’s your turn to pay.

Closing costs can vary based on the sale price, but in your starter home’s price range, the closing costs will be around $5,000. Often the seller will offer this sum to cover the buyer’s fees and put the amount in an escrow account that can be used to cover loan origination fees, mortgage application fees, appraisal fees, mortgage insurance application fees, attorney fees, title fees, and home inspection costs.

Remember when you, as the buyer, hired your home inspector and sent his or her laundry list of repair requests to the seller? Now it’s your turn to hire a handyman to fix your buyer’s wish list of repairs and improvements. The buyer's inspector might even find something critical that you didn't know about.

One of the biggest unknowns when selling a home is how long it will sit on the market. If you’re lucky, you will get an offer quickly and will only have to carry the mortgage a couple months while the inspections and paperwork are finalized. If your luck is not so good, you may have to make payments on your vacant home for months or even years after you’ve had to move into a new home. Home sales are not guaranteed, especially when dealing with a “starter home” that had such an attractive price when you bought it due to some of its less desirable qualities. You might be in a position where you need to attract just the right buyer in order to sell. Either way, however much you have to pay for your unused house while it sits on the market will effectively cancel out a portion of the equity you’ve put into it. Paying for a house you aren’t using is wasted money.

So in summary, your starter home will need to appreciate in value enough to cover the realtor commissions, closing cost fees, and at least a few extra mortgage payments, just for you to break even on the sale. All told, you could be out several thousands of dollars. That doesn’t take into account the time, energy, and stress it takes to complete the process while you’re in the process of moving to a new place and going through other life changes. Then, if the house does not sell quickly, you run the risk of losing several thousand more dollars and eating into your personal savings. Home sales are not a sure thing, and it can often take time to find the right buyer willing to take on your “starter home.”

These costs and risks of buying and selling a home are easier to shoulder when you live in the home for a longer period of time. Over time, as the principal of your loan gradually goes down, your interest payments start decreasing more rapidly, meaning more of your payment goes towards paying down your principal. And over a longer period of time, your home is more likely to appreciate comfortably in value than if you try to flip it after just a couple years.

Of course, if you’re handy and like fixer-uppers, improving and flipping homes can indeed be a profitable investment. But the notion that merely living in a house for a few years will make it appreciate enough to even cover the costs of selling it is usually just a fantasy.

Homeownership is a Beautiful Thing

We want to point out that we do not want to dissuade you from homeownership. Buying your forever home to build a life in and raise your family is a beautiful thing and something we wholeheartedly believe in. Indeed, that’s the American dream. And we also support living small and within your means to help establish your financial freedom. We simply want to warn our readers about the siren song of the “starter home,” which can sound like such a good investment in that surface-level sales pitch, but can actually end up draining your hard earned savings and delay your procurement of that dream home longer than necessary.

A good rule of thumb is to buy a home when you can see yourself living in it for 20 years. If you think you would only be in that house for a shorter time, it makes more sense to rent. By paying that little extra to rent a residence, you are effectively buying your freedom to relocate when you need to, worry-free. It may help you save enough to make that dream home a reality all the sooner.